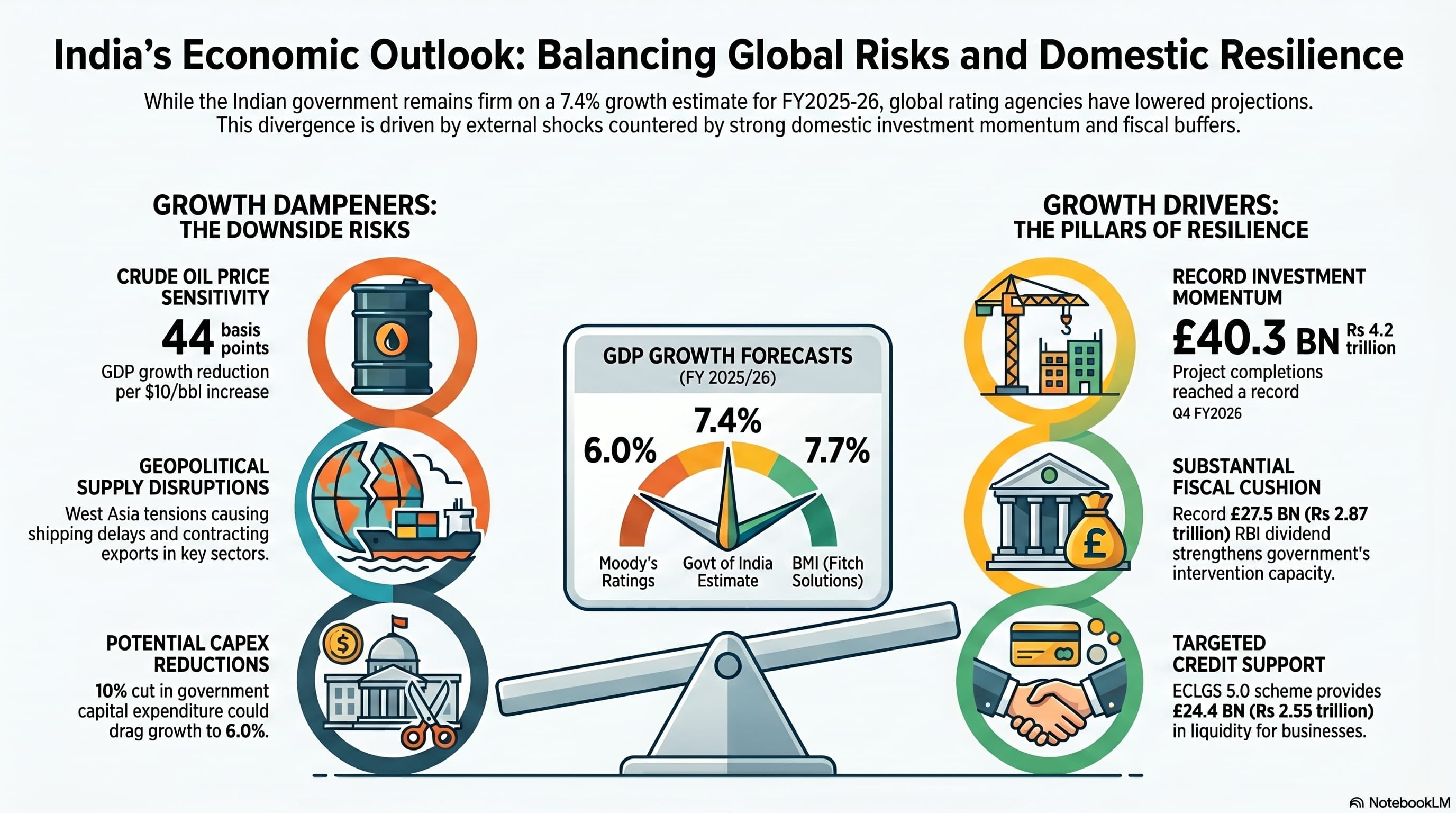

- Global agencies lower India’s growth; domestic outlook remains strong.

- Industrial and services sector growth slows amidst global uncertainties.

- Elevated crude oil prices pose significant risk to growth.

Nothing quite augurs for 7 per cent-plus growth for India in financial year 2025-26, going by the current indicators. Foreign portfolio investors (FPIs) continue withdrawing from Indian markets, resulting in net outflows of $7.6 billion in April. A depreciating currency amid weak capital inflows has kept the rupee under pressure, while input cost pressures have increased significantly for producers, which could drag GDP growth and push up retail inflation.

So, while a slew of global rating agencies and financial institutions have lowered their growth projections for India in the current fiscal, the Government and domestic stakeholders remain firm on a resilient 7.4 per cent growth estimate for 2025-26.

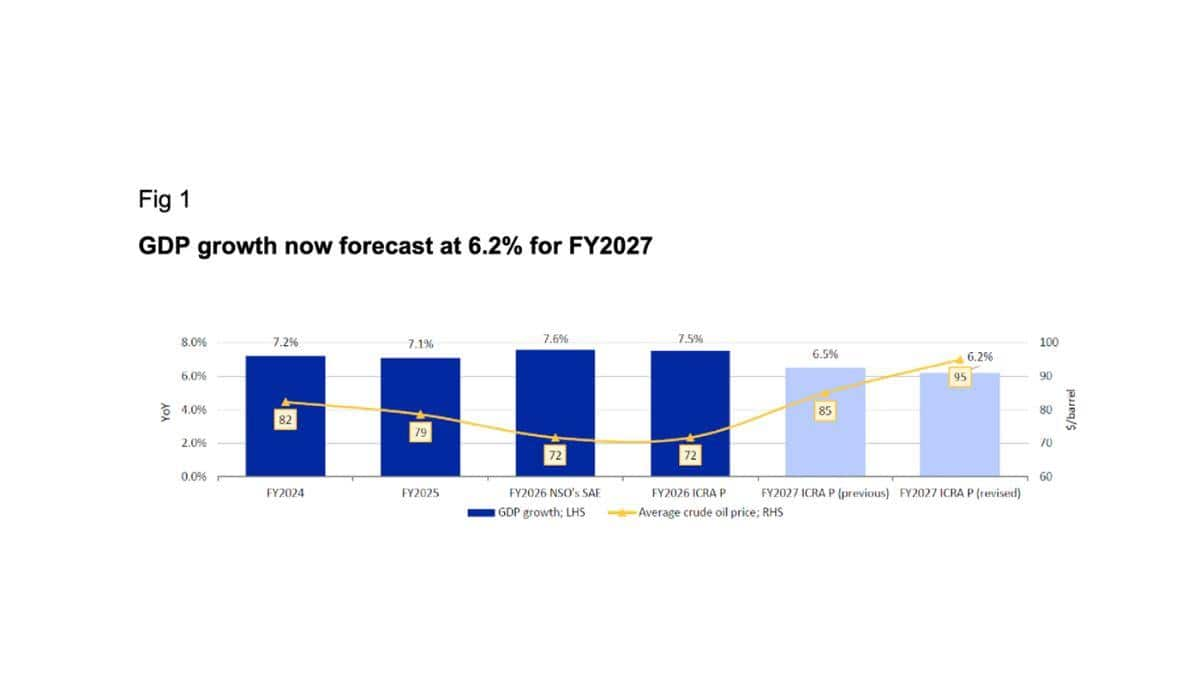

While ICRA projects year-on-year GDP growth at 7.0 per cent in Q4 2025-26 and 6.2 per cent in FY27, CRISIL, which has revised its India economic outlook as risks to resilience rise, now expects India’s GDP to grow 6.6 per cent and retail inflation to average 5.1 per cent.

Research from BMI (a Fitch Solutions company) expects India to grow 7.7 per cent in FY2025/26 and 6.7 per cent in FY2026/27. The Asian Development Bank (ADB), however, projects India’s GDP to ease to 6.9 per cent in fiscal year 2026 from 7.6 per cent in FY2025, while Moody’s Ratings has cut India’s GDP growth forecast for 2026 by 0.8 percentage points to 6 per cent, citing weak private consumption, slower capital formation and industrial activity.

Slower Industrial and Services Activity Raises Concerns

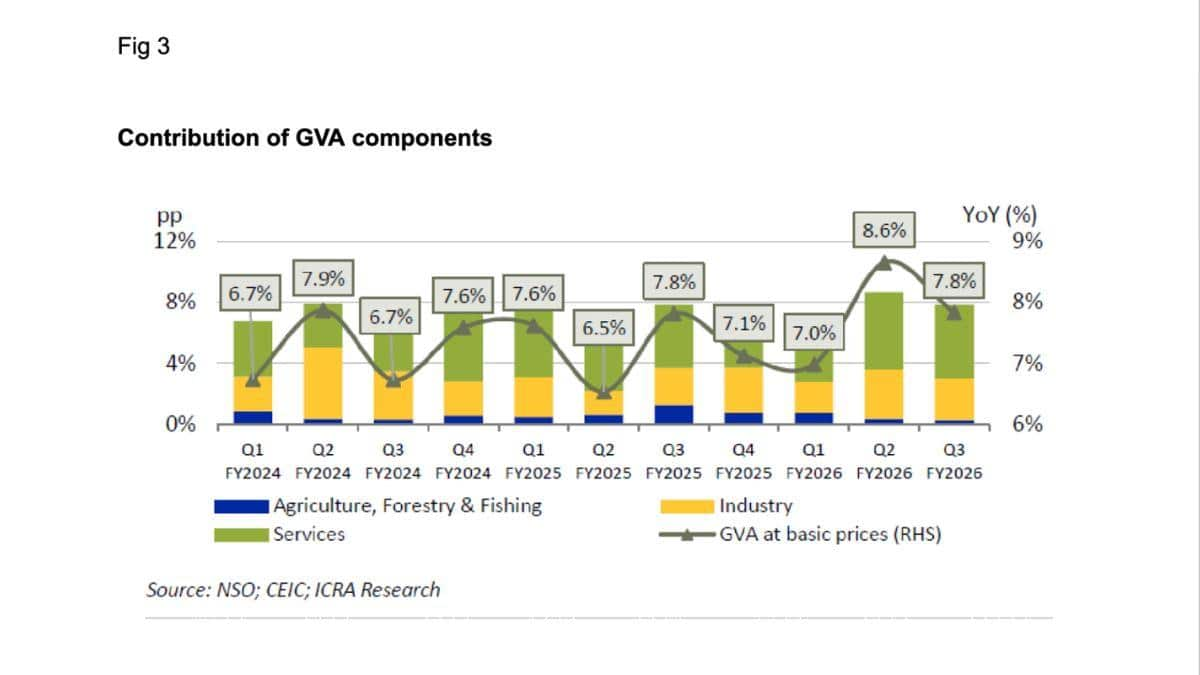

A slower expansion across the industrial sector, which saw 7.3 per cent growth in Q4 2025-26 against more than 9 per cent growth in Q3 2025-26, as well as a modest uptick in the services sector, which grew 8.5 per cent in Q4 2025-26 against 9.5 per cent in Q3 2025-26, is expected to have moderated GDP growth between these quarters.

The performance of most trade and transport-related indicators, such as port cargo traffic, domestic air passenger and freight traffic, and GST e-way bill generation, eased in Q4 2025-26 vis-à-vis Q3 2025-26, partly owing to disruptions caused by the West Asia crisis.

(See Fig 1)

Aditi Nayar, Chief Economist, Head – Research & Outreach, ICRA, notes that a slower rise in manufacturing volumes, contraction in exports, and nascent signs of margin pressure amid the West Asia fallout may have weighed on industrial gross value added (GVA) growth during the quarter.

Slowing global growth and shipping disruptions triggered by the West Asia conflict led to shipments of textiles, pharmaceuticals, and gems and jewellery contracting in Q4 2025-26.

The output of leather and related products contracted by 4.6 per cent month-on-month in March 2026 (versus an average of +3.9 per cent month-on-month during March 2022-2025), given the sector’s high dependency on petrochemical derivative imports from the region.

Based on available trends, ICRA projects manufacturing GVA growth to ease to 8-9 per cent in Q4 2025-26, falling to a single digit after a gap of five quarters.

As per ICRA estimates, GDP growth is pegged at 7.5 per cent in 2025-26, marginally lower than the National Statistical Office’s (NSO) second advance estimate of 7.6 per cent for the fiscal.

Also Read : Airfares, LPG, Solar Panels: 5 Financial Changes To Watch From June

Crude Oil Remains the Biggest Risk

India Ratings and Research (Ind-Ra) projects GDP growth at 6.7 per cent year-on-year in FY27, attributing higher fuel prices arising from uncertainty linked to the West Asia conflict as a key risk factor.

“A USD10/bbl increase in crude oil prices could reduce GDP growth by 44bp,” says Megha Arora, Director – Economics, Ind-Ra.

The agency’s baseline forecast assumes oil at $95/bbl and expects average prices of $110/bbl in Q1FY27, $100/bbl in Q2FY27, $90/bbl in Q3FY27 and $80/bbl in Q4FY27.

“If oil prices average $120/bbl, the growth could decline to 5.6 per cent,” warns Arora.

Crude Price Shock and Macro Stability

The international price of crude oil (Indian basket) stood at $114.5/bbl in April 2026 following the escalation of the West Asia conflict and resulting supply disruptions.

Thereafter, prices eased by 6.8 per cent sequentially to $106.7/bbl during May 1-15, 2026, although they remained above the $100/bbl mark, posing a threat to India’s macroeconomic stability because of the country’s dependence on imports for key energy products and fertiliser inputs.

“We now assume crude oil prices to average at $95/bbl in FY2027, against our prior estimate of $85/bbl, given the ongoing stickiness in prices amid the stalemate in West Asia. Consequently, we have pared our baseline forecast for FY2027 GDP growth (at constant 2022-23 prices) to 6.2 per cent from the 6.5 per cent expected earlier,” Nayar added.

(See Fig 2)

Given the uncertainty surrounding the conflict’s resolution, elevated energy prices over an extended period pose downside risks to growth, including weaker investment demand, pressure on corporate profitability and dampened consumer sentiment.

Also Read : Scanned A Fake QR Code And Lost Money? Here Is What You Must Do Right Now

Capex Cuts Could Further Hurt Growth

A major domestic dampener to GDP is weaker-than-expected capital expenditure, particularly by the Government as it seeks to manage fiscal risks.

A 10 per cent reduction in government capex from the base case could pull FY27 GDP growth down to 6.0 per cent, according to Arora.

The Government may defer capex spending to control the fiscal deficit.

Significantly, Ind-Ra notes Prime Minister Narendra Modi’s appeal for austerity by both the Government and citizens. If this translates into a 10 per cent reduction in government capex by both Union and state governments, Gross Fixed Capital Formation (GFCF) could slow to 5.2 per cent and drag GDP growth down to 6.0 per cent in FY27.

(See Fig 3)

Rural Demand Shows Early Signs of Stress

Rural demand, a key growth indicator, weakened towards the end of Q4 FY26 as sentiment took a hit.

According to the RBI’s Rural Consumer Confidence Survey (RCCS), the Current Situation Index (CSI) for rural and semi-urban households declined sharply in March 2026 following the escalation of West Asia tensions, reflecting concerns around gas and fertiliser availability and the potential emergence of El Niño conditions.

The index had remained in positive territory until January 2026 before reversing after six consecutive survey rounds.

Interestingly, FMCG players highlighted that rural demand remained steady in Q4 FY2026. However, margin visibility was mixed depending on raw material exposure, reliance on crude-linked inputs and the ability to pass on costs, factors that could weigh on demand sustainability in the near term.

Why Some Agencies Remain Optimistic

Research from BMI expects India to grow 7.7 per cent in FY2025/26 and 6.7 per cent in FY2026/27.

While the FY2025/26 forecast represents a 0.1 percentage point upward revision from the previous estimate, the FY2026/27 outlook remains unchanged.

One reason is the assessment that the impact of last year’s tax reforms will fade by Q2 2026. This trend is already visible in vehicle registration data, which showed new registrations growing 9 per cent year-on-year in April after increasing 23 per cent in Q1.

Higher income levels generated by last year’s strong GDP growth are also expected to support imports during FY2026/27.

Government Bets on Investment Momentum

The Government is looking to investment trends for support.

Investment activity remained largely favourable in Q4 FY2026, with project completion reaching a record Rs 4.2 trillion, compared with Rs 2 trillion in Q3 FY2026 and Rs 2.8 trillion in Q4 FY2025.

Additionally, capital spending by the Centre and 26 state governments rose by 12 per cent year-on-year during January-February FY2026.

Also Read : Gold Silver Rate Today (May 29): Prices Fall Nearly 1%, Check Latest Rates In Delhi, Mumbai, Chennai, More

Support Measures for Industry and Trade

The Government’s optimism is also supported by measures aimed at helping businesses weather the crisis.

The Emergency Credit Line Guarantee Scheme 5.0 (ECLGS 5.0), approved by the Union Cabinet, covers both MSMEs and non-MSMEs with a targeted credit flow of Rs 2.55 trillion, including Rs 50 billion earmarked for airlines.

The scheme provides 100 per cent guarantee coverage for MSMEs and 90 per cent for non-MSMEs, helping borrowers manage liquidity pressures arising from the West Asia crisis.

RBI Dividend Provides Fiscal Cushion

Nomura economists Aurodeep Nandi and Sonal Varma point out that the RBI transferred a record Rs 2.87 trillion dividend (0.75 per cent of GDP) for FY26, compared with Rs 2.69 trillion in the previous year.

“This has broadly been in line with our expectations, and the estimates in the FY27 Union Budget, but short of some market expectations of a bumper transfer of Rs 3.0 trillion,” they said.

This provides the Government with an important buffer against fiscal risks.

Devendra Kumar Pant, Chief Economist, Ind-Ra, believes the surplus transfer will strengthen the RBI’s ability to intervene in financial markets amid evolving domestic and global macroeconomic conditions.

Weather, Rupee and the Road Ahead

Policymakers and economists continue to believe that while India remains vulnerable to high crude oil prices and deficient rainfall, vulnerability to rainfall has reduced over the years because of higher irrigation coverage, improved agricultural extension services, a larger share of allied agricultural activities and the increasing contribution of services to GVA.

If rainfall distribution between June and September remains close to normal, risks to agricultural GVA could be contained.

Experts expect the rupee to average 93.5 per US dollar in March 2027, compared with 92.8 in March 2026, amid heightened volatility.

Although India’s external vulnerability has increased because of a widening current account deficit and foreign capital outflows, many analysts expect the rupee to strengthen from current levels towards the end of the fiscal year if geopolitical tensions ease.

This would be consistent with historical currency cycles, where periods of sharp weakness are often followed by a gradual correction.

{kind=link}